IBM is looking for trouble… or at least fraud. The company purchased Iris Analytics, a company that developed a real-time fraud engine for machine learning. I guess Watson really will be Watson-esque. IBM also topped US patent creation list (again).

HPI did not have good news during the holidays, PC sales slipped (except for Apple), while HPE looks to sell of their stake in MPhasis ($1B).

EMC has a new CIO and Microsoft dropped their cloud fees to be more competitive with Amazon.

IBM

- IBM buys fraud sniffing biz for real-time protection

IBM has assimilated a German payment fraud prevention business, IRIS Analytics, a provider of a real-time fraud analytics engine using machine learning algorithms, for undisclosed terms.

http://www.theregister.co.uk/2016/01/15/ibm_slurps_up_fraud_detection_biz_for_realtime_protection/

- IBM tops US patent list again

The computer company was granted 7,355 patents in the US. According to its statement, IBM inventors generated more than 2,000 patents in areas related to cognitive computing and the company’s cloud platform.

http://ipprotheinternet.com/ipprotheinternetnews/article.php?article_id=4738

- IBM Introduces Dynamic Pricing to Help Retailers Navigate Online Price Wars

“At any given moment, a retailer is no more than one click away from losing a customer online. IBM Dynamic Pricing executes real-time pricing recommendations at the scale and speed needed to ensure competitiveness in a volatile shopping environment,” saidStephen Mello, Vice President, IBM eCommerce & Merchandising. “This intuitive and dynamic pricing system improves visibility into what’s happening in the market, allowing retailers to make decisions that are best for their businesses and customers alike.”

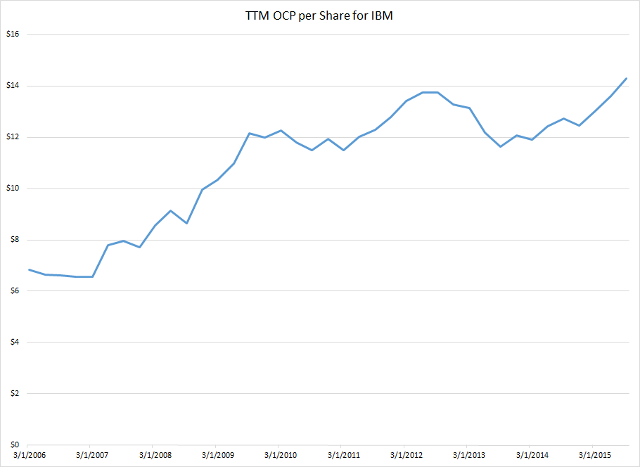

- IBM’s Profits Hit An All-Time High

While stagnant on a nominal basis, IBM’s per-share profitability has hit an historical high in the most recent trailing 12-month period. This improvement can be attributed to two factors: value-accretive share buybacks and the firm’s shift in focus to less asset-intensive businesses. Uncertainty remains as to how soon the company will be able to generate revenue growth, but growth in profits and cash flow are arguably more important to valuation.

http://seekingalpha.com/article/3810366-ibms-profits-hit-an-all-time-high

More on this:

Outstanding! In fact, IBM’s profit per share increase works out to roughly a 9% compound annual growth rate of profits since 2006 and the most recent trailing twelve-month figure is the highest in the company’s history.

HP Inc | Hewlett Packard Enterprise

- Apple leads holiday PC shipments despite market contraction

Market leaders Lenovo, HP Inc. and Dell all faced decreases, with Lenovo’s shipments declining to 15.4 million from 16.1 million, HP’s dipping to 14.2 million from 15.4 million and Dell’s dimming to 10.2 million from 10.8 million. The fourth quarter marked the fifth straight quarter of worldwide PC declines, and Mikako Kitagawa, principal analyst at Gartner, said holiday sales “did not boost” the market.

http://www.forextv.com/market-news/apple-leads-holiday-pc-shipments-despite-market-contraction/

- HP Inc. Is Cheap, But Is That Enough?

In the medium to longer term, it’s also worth thinking about whether the strong improvements in battery life enabled by newer generations of chips will continue to extend the refresh cycle over time. Think about it – old laptops that had 2-3 hour battery life to start with left you with battery anxiety within a few years. Now that smaller, more power-efficient laptops can get double or triple that battery life, there may not be as much need for personal users to replace laptops as quickly. This article from Digital Trends demonstrates the rapid improvements in battery life over just the past few years – and indications are that Intel’s Skylake chips will continue the trend of Haswell and Broadwell toward greater efficiency.

http://seekingalpha.com/article/3803146-hp-inc-is-cheap-but-is-that-enough

- Hewlett Packard Enterprise (HPE) to Sell ($1B) Stake in Mphasis?

Hewlett-Packard purchased Mphasis when it acquired Electronic Data Systems in 2008 for approximately $13.9 billion. At the time, the company’s Technology Solutions Group segment shifted its outsourcing services operations and a part of its consulting and integration activities to Electronic Data. The Indian company has since functioned as an independent subsidiary of Hewlett Packard. The sale of Mphasis comes at a time when the company is attempting to restructure its IT consulting and services group. Hewlett-Packard stated that it was planning to shed around 25,000 to 30,000 jobs in its enterprise business.

http://www.zacks.com/stock/news/203493/hewlett-packard-enterprise-hpe-to-sell-stake-in-mphasis

EMC | Dell

- EMC gets new CIO in midst of Dell purchase

ML Krakauer took the reins as EMC’s CIO last week, replacing Vic Bhagat, who joined EMC as CIO in 2013.

http://www.ciodive.com/news/emc-gets-new-cio-in-midst-of-dell-purchase/411931/

- How Will EMC’s Once Pivotal Ambitions Play Out?

To be fair, that may never have been Pivotal’s vision, though there’s little question that EMC and VMware had to offer their customers a reason to stick with their more expensive, proprietary solutions instead of rushing to Amazon. Whether they succeeded with that is unclear, but we’ll leave it to Michael Dell to craft the rest of that story. Pivotal, on the other hand, may have the chance to write its own story if reports of its immanent IPO are true. In the mean time, it went shopping — but more on that later.

http://www.cmswire.com/information-management/how-will-emcs-once-pivotal-ambitions-play-out/

- EMC exec reacts to criticism of proposed Dell merger

“Vinod is a smart venture capitalist and I don’t doubt his ability to recognize innovation in startups, but his view on our ability to innovate at scale is not entirely accurate,” according to a Tuesday filing with the U.S. Securities and Exchange Commission. ” … As a roughly $80B entity, Dell+EMC will need more than just one source and method of innovation. Our model provides exactly that.”

- EMC’s Stock Fell 14% in 2015

the share price of EMC fell 14% in 2015 from $29.83 to $25.68. Its share price fell 6.2% on October 21, 2015, as it reported an 8.3% YoY (year-over-year) drop in EPS (earnings per share) in its 3Q15 earnings results. Its reported revenues of $6.1 billion were in line with analyst estimates.

Other

- Microsoft Drops Prices For Some Azure Instances By Up To 17%

Microsoft has long said it would match AWS’s prices for compute, storage and bandwidth. Earlier this month, Amazon dropped the priceof some of its general purpose, compute- and memory-optimized EC2 machines. It doesn’t come as a major surprise then that Microsoft is now also dropping the prices for some of its virtual machines by between 10 and 17 percent.

http://techcrunch.com/2016/01/14/microsoft-drops-prices-for-some-azure-instances-by-up-to-17/

Photo: Greg Rakozy